Yves is Flinks' Content Strategist. He tells the world about the dramatic changes happening in finance, one story at a time.

How to Win the Fight for Consumer Trust — Trust Us, You Can

All successful personal and business relationships rely on the elusive, complicated human quality of trust. In a crowded financial marketplace, trustworthiness is a key differentiator and a driver of loyalty.

To help you get started (or get serious) about building trust, we’ve gathered insights and practical strategies from leading trust experts.

Save these insights for later. Download as a pdf.

Finance is founded on trust. Bankers in the gold rush era built the largest, most solid structure in mining towns to signal protection against outsiders — but also to assure clients that they did not plan to bolt overnight with their savings.

Today, trust is digitized; customers are more preoccupied by firewalls than physical walls. Banking customers rarely enter a branch, let alone worry about its size.

How our brains decide when to trust

While approaches to customer trust have evolved with time, the human psychology that underlies it remains constant. Trust revolves simultaneously around competency and reliability, as well as a suite of harder-to-measure drivers that include power dynamics, shared risk, reciprocity, intentionality and character.

“When we want to trust an individual, company, or any agent, we make an assessment,” explains Paul Marsden, consumer psychologist and head of insight at global digital marketing company Syzygy.

“The first thing is their competence: Are they able to help me? The second thing is their intention: Do they want to help me and do they care about me?” — Paul Marsden, Syzygy

While the financial services sector is broadly perceived as competent – despite the crash, it continues to be the choice handler of the world’s money – it flunks part two of Marsden’s test. The sector has repeatedly come bottom of all the major industries featured in an annual trust barometer published by management consultancy Edelman. In the 2019 scorecard, just 57 percent of 33,000 respondents said they trusted the industry.

In another survey of nearly 20,000 adults across 27 countries by British market research firm Ipsos Mori, 52 per cent of respondents said they felt that banks would take advantage of them if they could.

“There are different types of trust going on here in relation to financial services,” explains Colin Strong, global head of behavioural science at Ipsos Mori.

“The extent to which we trust them to look after our money and not to mess it up is one thing. The degree to which we consider them to be trustworthy is another matter.” — Colin Strong, Ipsos Mori

Sidenote: here’s why trust should be on your radar

Financial service providers collectively face the challenge of graduating from a basic level of customer trust – one where they are deemed competent, albeit self-serving – to a more active, interactive and productive level of trust. To beat off competition in an increasingly crowded marketplace, they need to offer these new types of customer experiences.

Thankfully, the current era of data connectivity and analytics offers up a suite of new strategies to garner enhanced trust. Open banking — adopted in the UK and Australia, and much needed here — provides an opportunity for financial service providers to foster customer trust by giving them more agency and power over their financial data.

Otherwise traditional financial service providers risk being left behind.

Strategy #1 — Design with care in mind

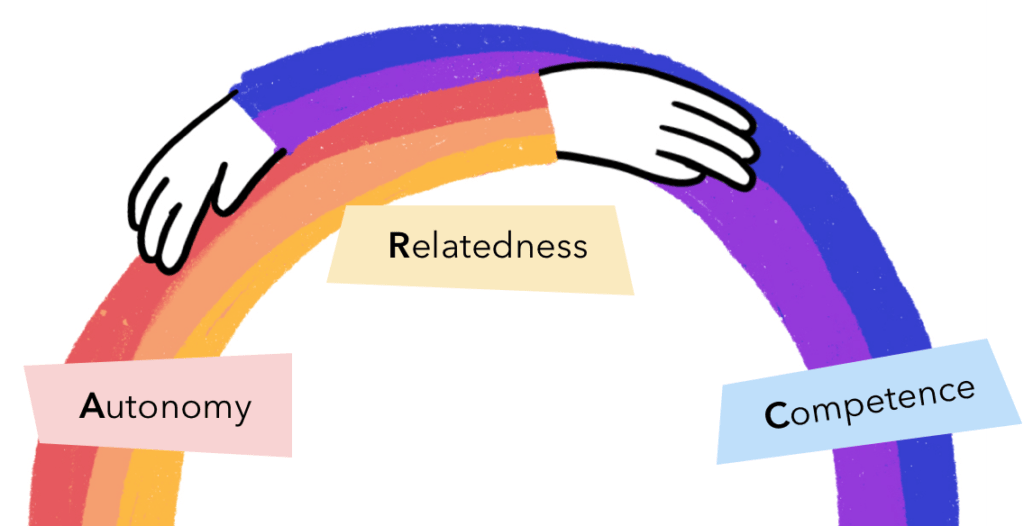

Financial businesses should engineer their offerings and services to give customers a sense of autonomy, a sense of relatedness and a sense of competency, according to Marsden, who also lectures at the University of the Arts, London.

“The ‘ARC of happiness’ is the most validated framework for human well-being in psychology,” he explains. “The A stands for autonomy, the idea of agency and feeling in control. The R is for relatedness – we are born alone, we die alone, we spend most of the intermediate time trying not to be alone, that kind of thing. The C is a sense of competence, we need to feel smart or made smarter by the service or product.”

“Companies hoping to build and maintain trust should be catering to all three.” — Paul Marsden, Syzygy

Marsden laments the fact that most financial service providers are currently prioritizing technological proficiency and innovation at the expense of thinking about customers’ financial well-being.” “Everyone is focused on competencies right now – on tech, on algorithms, on AI, etc – rather than demonstrating that they care about the financial well-being of the person they are seeking to serve,” he explains.

“From a basic psychological perspective, there’s a huge missed opportunity and indeed a huge cost for financial services that go down the technology route, the features route, or the benefits route, without actually showing that they care.”

Open banking could and should be engineered to this end, explains Marsden. It has the potential, when applied correctly, “to empower customers to make better financial decisions for their own financial well-being.”

The regime gives customers greater control over who can access and use their personal data, as well as a more informed oversight of their financial decision-making.

Strategy #2 — Share risks, reap mutual rewards

Shared risk is a much-overlooked component of customer trust in brands, according to Ipsos Mori’s Strong. He says that companies would be wise to pay it heed and resist the urge to focus myopically on risk mitigation.

When dealing with customers data, service providers need to demonstrate “clarity, transparency and being clear about what the value exchange is. Is it fair?” he explains.

“If I (the customer) am going to trust you (the firm), what skin do you have in this game to make sure everything’s okay?” — Colin Strong, Ipsos Mori

Major fashion retailers, for example, provide the option for clothes to be returned. It’s a system that could easily be abused. But in the end, it boosts customer trust and company profit.

“If you actually take a risk, you may find a small number of (customers) will abuse that, but that the majority of them respond positively to it,” Strong explains. “If you are investing your trust in somebody else, they are more likely to do right by you, to do the right thing. That is not often understood or undertaken in today’s business climate.”

Strong points out that trust and transaction are often confused.

“A transaction is: If I do this, you’ll do that. That’s not a trusting thing, that’s a transactional thing. Whereas if you say: If I do this and I hope that you’ll do something for me in return – that’s what allows trustworthiness to develop,” he explains.

“You can’t mandate that. It’s in the gift of the individual to decide whether or not they’re going to consider you to be trustworthy. And that’s what makes it this kind of elusive, fascinating and fundamentally human quality.”

You might also like

Your Competitors Are Turning to Transactional Data, Here’s Why

The banking industry is undergoing disruption, driven by shifts in culture and technology. Here’s an (extremely) short list of what you need to do to win.

What Your Customers Are Thinking About When They Get Asked to Connect With Flinks

As more and more consumers connect their bank accounts to financial apps and services, some want to learn more about the technology enabling them to do so.