Flinks gives you the power to build the future of finance. Connect, enrich and utilize financial data to delight your customers with amazing products.

Investing in their own future: Why an investing app chose Flinks

Automated savings and investing apps bring real solutions to a challenge many consumers have been facing for years: putting money aside regularly to reach their financial goals as painlessly as possible. Their benefits are highly tangible and often wrapped in a delightful digital experience, which makes them a very attractive option for consumers.

One of Flinks’ clients is a leading provider in this space. Their app operates on daily connections to their users’ bank accounts, making them highly conscious about the importance of working with a reliable data aggregation partner.

Read on to learn how this client uses Flinks’ Digital KYC feature to convert users faster and drive long-term retention.

Objectives

- Improve conversion rates

- Reduce churn

Approaches

- Get users to value faster with a fast and seamless onboarding experience

- Improve bank account linking to encourage users retention

Benefits

- Instant onboarding

- Lower drop-off rates

- Lower cost to convert

Save this case study for later. Download as a pdf.

Need for speed… and fresh data

This client needs financial data for two main reasons:

- To onboard their users faster, by making identity verification a quick, digital and automated process — instead of using other digital options that add friction to the experience, such as reviewing bank statements;

- To have access to a steady stream of fresh data in order to perform at its best capacity for their users.

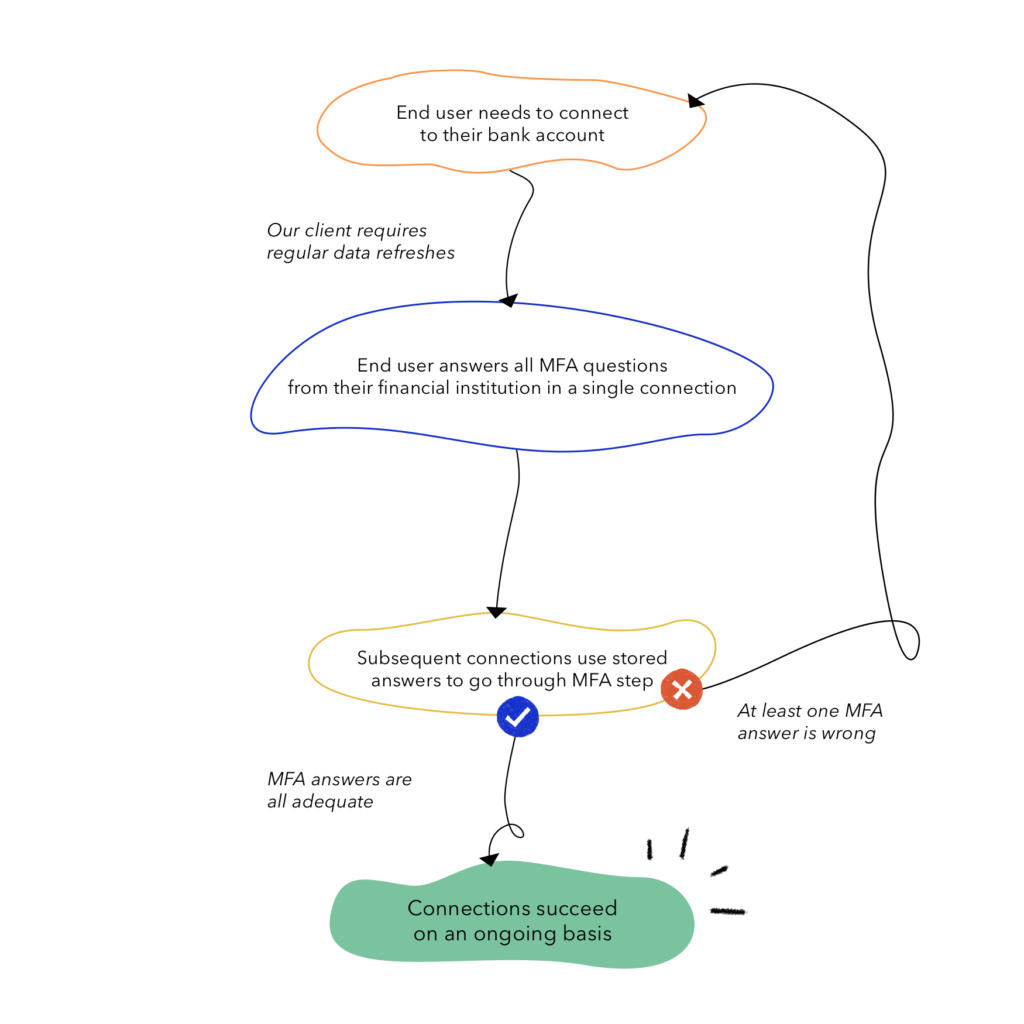

What our client wanted was for their users to connect only once and never have to go through the connection flow again.

Refreshes would run in the background to provide the critical information needed by the client to operate at optimum rates, making for the seamless user experience intended.

It’s no secret that the end user retention rates for financial apps can be crippled by issues with bank account linking. Two scenarios are especially common: changes on the bank’s side preventing a connection to its online or mobile platforms, and MFA (multi-factor authorization) disruption breaking the seamless refresh experience. When connections to bank accounts break or fail, financial apps can’t function properly and must prompt their users to connect again.

Achieving this requires using a robust data connectivity service.

The client knew from the get-go that building a seamless and stable experience was critical to convert more users, and further still, to reduce churn — if users disconnect, chances are high they won’t reconnect.

However upon investigating their options, our client realized that many providers were lacking solid connections, be it for their high kick-out rates or because of their overall low success rates. This client wanted to grow with a safe, secure and sturdy partner that offers solid linking to bank accounts, which is why they turned to Flinks.

Getting up to speed

Flinks Connect

When they reached out to us, our client was still in the beta phase of their platform. Being able to work with their team at such an early stage allowed us to provide useful insights and technical guidance on how to best integrate financial data connectivity.

Upon meeting with their team, through detailed-oriented consultative work, we concluded that the best and easiest way for them to benefit from our product would be to use the Connect interface, which is a turn-key solution of our API that requires minimal integration. The widget’s experience uses customized wording that matches each Financial Institutions’ connection experience — it guides users through a simple and intuitive process to authorize a connection to their bank account, and handles edge cases.

Digital KYC

To accelerate their identity verification process, our client uses the information from our Digital KYC feature.

Indeed, banks already identify their customers when opening new accounts, and the identity information they hold can be leveraged to perform KYC checks. This is why many financial service providers require their users take the extra step of uploading a bank statement as a verifying method.

Digital KYC speeds up that process: when our client’s users go through their onboarding process and connect to their bank account, our client can automatically get a positive or a negative match on their identity.

Constant Fine Tuning

Expectation management is also essential to ensure the client’s satisfaction with our product, long after the integration is completed. It was important to educate this client on two major points:

1) no bank account linking is entirely foolproof — despite having a very high average success rate of more than 98.5%, not all connections will go through. Building a reliable product involves constant fine-tuning in order to make the success rate as close to perfection as possible.2) disconnections will happen — it’s a reality we have to deal with, and that can come from multiple factors, be it changes on the financial institution’s side, wrong answer to an MFA question or a handful of other factors.

One thing our team did was to guide our client as they built a user experience that takes that disconnection possibility into account and guides the users towards a reconnection.

We’ve also found that the key is lower disconnection rates to a minimum was constant fine- tuning of our product as well as whitelisting partnerships with financial institutions. We’ve documented the measures we’ve put in place to ensure high reliability. Over the years, we worked closely with our client to improve two key performance indicators (KPIs):

- Average time to connect

- Drop off rate

Since there was no precedent to compare the numbers that were acquired during the testing phase, our client simply compared them to our competition, to have a clear portrait of which aggregator was better. Ultimately, the numbers looked like this:

- Average time to connect: 19.4 seconds, with more than 80% of connections taking less than 15 seconds

- Drop off rate: 6.93% average among all institutions

Full Tilt

After implementing Flinks to their customer onboarding process, our client’s performance has seen a major increase in adoption, accompanied by a very low churn rate.

This indicates two things: users love the platform, and they (mostly) do not get disconnected from their bank’s linking.

Collaborating with this client’s team from the get-go helped us help them opt for the best integration. We ensured as little disruption as possible during the integration and enabled them to power their data-driven processes quickly. We were also able to educate them on what could be achieved with financial data aggregators, making sure that their satisfaction level remained high long after the integration of the product was completed.

Human to human connections, constant communications and open communication channels between both teams made this partnership a success.

If, like our client, you would like to build your product on seamless bank account connections and robust data refreshes, talk with our experts. They will be able to guide you on how to deploy financial data connectivity in the context of your business.

You might also like

How NCR Financial Uses Flinks to Improve Lending Underwriting

Digital lender NCR Financial uses Flinks to gather its customers’ transaction history and make instant, automated underwriting decisions.

How Wise Uses Flinks to Activate Customers and Reduce Risk

Wise delivers instant and convenient money transfers (EFT). Here’s how Flinks helps make it happen.