Yves is Flinks' Content Strategist. He tells the world about the dramatic changes happening in finance, one story at a time.

How NCR Financial Uses Flinks to Improve Lending Underwriting

A question for the ages: how do you create a truly convenient customer experience? This is the challenge that keeps NCR Financial focused on bringing innovation in digital lending. From automated underwriting to staying engaged with its customers every step of the way, NCR puts data to work.

Dustin Canuel, Chief Operating Officer, explains how Flinks helps make it happen with Transaction History and Instant Digital KYC.

Bring this case study home and use it anywhere. Download as a pdf.

Data-driven digital lending

Consumer lending exists to help people move more rapidly towards goals that range from paying for medical and housing repairs costs to dealing with unexpected emergencies. Yet, one in four Americans do not deal or cannot get a loan with a traditional bank. For consumers with no credit or low credit scores, this lack of access to financing translates into lost opportunities or worse.

Enter NCR Financial, a digital lender operating in Canada and the United States. As with all lenders, NCR faces one fundamental question: how to best predict a borrower’s ability to repay.

“With better intelligence, we make better decisions. Flinks helped us lower our default rate.”

When underwriting borrowers with average or limited credit history, conventional means of gathering information and assessing creditworthiness fall short. “A credit bureau doesn’t help me,” says Dustin. “More and more we’re looking at the immediacy of what’s happened in their banking situation in the last 90 days versus what’s happened in the credit bureau last year.”

While millions of people with no or low credit scores pay their rent and bills on time, that information takes a long time to be captured by traditional credit scoring.

Using Flinks’ Transaction History, NCR automatically receives the up-to-date information they need. “When we use a customer’s transaction history data to analyze their financial situation, the loans perform better than a traditional credit bureau model”, explains Dustin. With reliable and comprehensive data to feed their models, NCR’s underwriting team can make sure borrowers fits their requirements.

Quick process, instant decisions

NCR knows its customers don’t want to wait. In fact, no one wants to wait: by now we all have high expectations when it comes to quality customer experience. But there’s more to it. A customer taking a personal loan has weighed their options and is ready to act. A key differentiator in digital lending is the ability to deliver loans instantly.

The secret is automated underwriting.

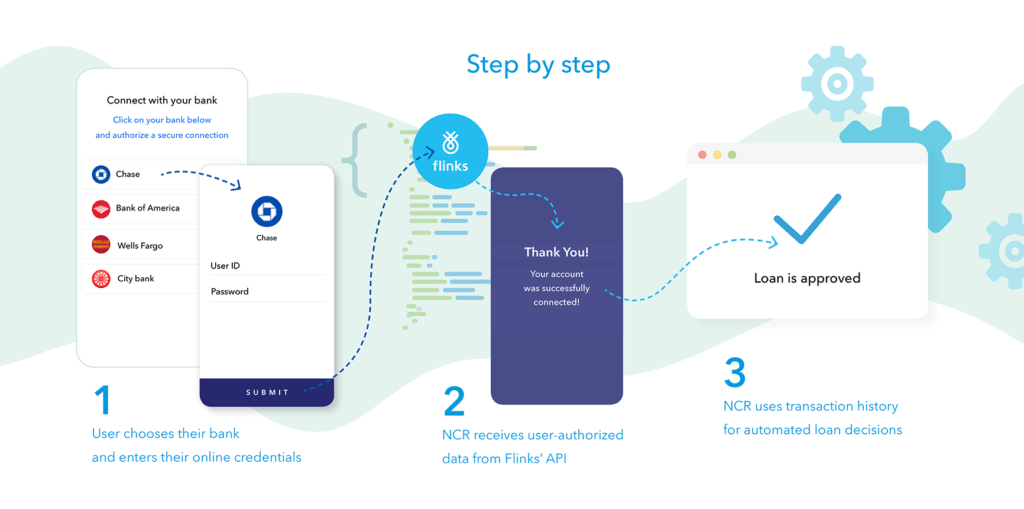

And financial data connectivity allows just that. Integrating Flinks directly into its digital experience enables NCR to build a quick and efficient process. In just a few steps, loan applicants connect their bank accounts to validate their identity and authorize access to their transactional data. Loans can be approved in minutes.

“Flinks allowed us to automate and scale a previously manual process.”

Transaction history data flows seamlessly into NCR’s risk models, making them powerful tools for automated decisions. “Flinks makes it possible to have the immediate customer situation,” Dustin says. “We are able to make an instant decision and provide the money to the customer swiftly.” NCR’s risk experts can focus on cases that require close attention.

Top tier customer experience

Looking ahead, Dustin Canuel has plans to solve other problems using Flinks. “More and more we are focused on being a fintech-type organization,” he explains. Financial data connectivity allows him to approach the lending process with an innovative mindset.

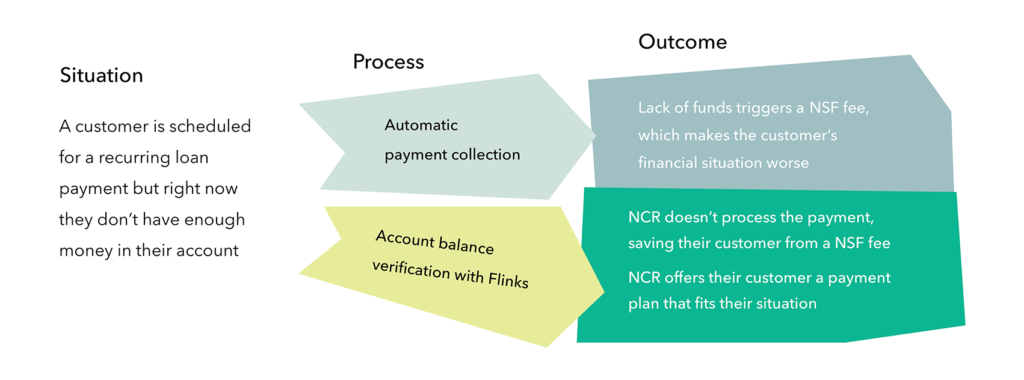

One area ripe for improvement is payments collection. NCR’s customer-centric vision is all about being proactive in offering a painless experience when it is time to collect money. Traditionally, scheduled payments were a shot in the dark. Hopefully, the client has the funds in their account — but not knowing can trigger a bank fee for returned payment.

NCR is currently developing its ability to leverage Flinks in order to verify its customers’ account balance before processing a payment. Understanding its customers’ situation in real-time will allow the lender to protect them from NSF fees.

With this new feature, says Dustin, NCR will deliver a unique customer experience: “We’re going to be able to say ‘We’re not going to take your payment because we know you don’t have the money in your account. Can we make a better arrangement that fits your current situation?’”

Clever use of new technology allows for creative problem-solving, better processes and industry-leading customer experience.

You might also like

The digital transformation of the KYC allows financial businesses to fight fraud, customer attrition, and business risks more efficiently.

How TransferWise Uses Flinks to Activate Customers and Reduce Risk

TransferWise delivers instant and convenient money transfers (EFT). Learn how Flinks helps make it happen.