Simon-Pierre is Flinks' VP of IT Operations & Security. He's the person that makes things work.

What Your Customers Are Thinking About When They Get Asked to Connect With Flinks

This article addresses a series of questions that can come to consumers’ minds as they are sharing information by connecting to their bank account.

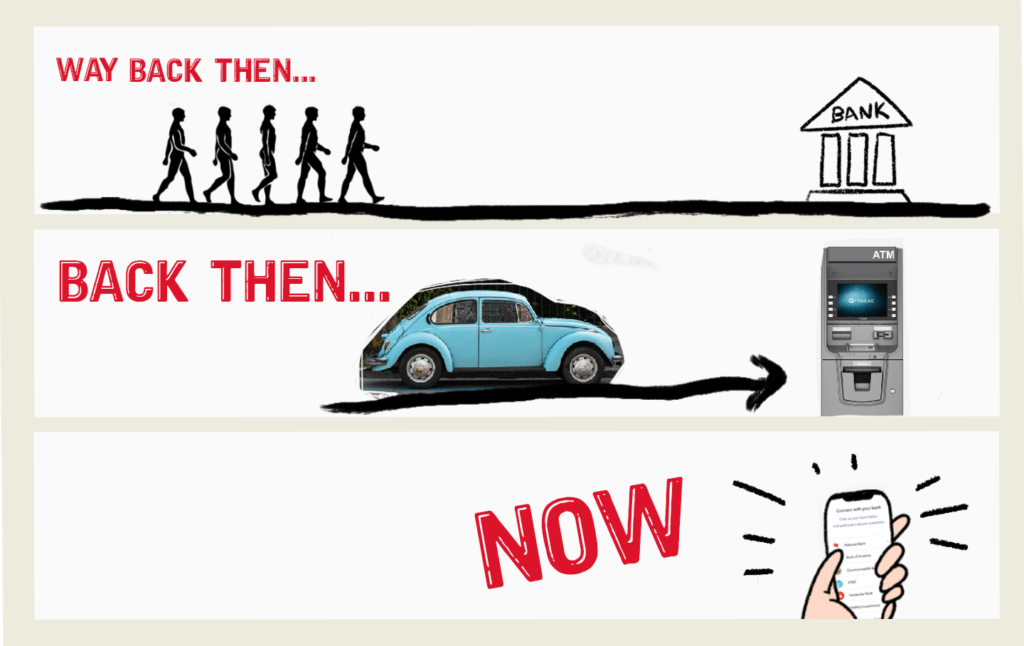

Our grandparents had to meet in person with bank clerks. Our parents drove to an ATM. We now move money whenever and wherever we want all the at the tip of our fingers. The face of financial services is changing dramatically.

However, we rarely get to see the technology powering these changes — so let’s talk about it.

TL;DR [Too long; didn’t read]

- Connecting to bank accounts is a thing now. Financial providers everywhere, from startups to traditional institutions, have adopted this as a new way to collect information — allowing you to access the financial services you want in virtually one click.

- Connecting with Flinks is a safe way to share information. Consumers connecting their bank account get the same level of security that they do when they connect to their financial provider.

- Finance only gets better from here. Financial providers have always needed to collect information to verify your identity and assets. But smart companies are now using the information you share to build better features and provide a more personalized experience.

“Why did an app ask me to connect with Flinks?”

The short answer is that connecting to your bank account is the latest way an app — or any financial provider, really — can get the information it needs to deliver the service you want.

Understanding why a business would want information sourced from your bank account requires a longer answer that starts with a question: Remember bankbooks? Do you still use cheques? When was the last time you made a cash deposit?

Granted, that was more than one question. But they all point in the same direction: everything is happening online now. Even finance can’t escape that.

To give you access to a service, most financial businesses need to verify your identity. Many need to assess your financial health. In short, they need information about you.

Yes, you can scan and upload bank statements or tax returns. But we live in a world where launching a car into space is possible. So surely there is a better way.

This is why we exist.

We are the pipes and plumbing connecting apps to bank accounts, millions of them, all at the direction of consumers like you. Our technology is used by digital pioneers like Wise, a money transfer service, and KOHO, a fully digital bank. But you’d be surprised how many banks, insurers, mortgage brokers and other more traditional institutions use Flinks too.

They come to us so they don’t have to think about all the technical stuff that goes into connecting to bank accounts. They trust us to create that simple and secure way for you to share the information they need to provide their services.

A major outcome is that moving money, getting a loan or verifying your identity to sign up to that trading app you like is becoming substantially more convenient for you.

“You just mentioned security. Is Flinks safe?”

Yes.

“How can you be so sure?”

We rock industry-leading levels of security to keep your information safe and secure.

It’s your information, not ours. So when it comes to privacy and security, we need to be up to the highest standards — yours.

It’s not just the right thing to do. It’s the only way millions of people can trust us with sharing their financial information where and when they want to.

We’re transparent about our practices. Here’s a plain language summary:

- We make sure that no one can access your information without your knowledge and permission.

- We protect all sensitive information using the latest encryption algorithms. When we do need to store it, it’s on servers sitting comfortably on national soil.

- Our security controls are routinely audited by independent firms as well as some of the biggest financial institutions. In fact, we successfully passed a SOC 2 Type II examination. And before you Google it: SOC 2 is the gold standard for companies handling their customers’ information.

- We understand security doesn’t stop at our door, so we make sure we can trust our own clients to take good care of your information.

- Everything we do surpasses the requirements of PIPEDA, Canada’s federal privacy and data protection law.

Financial businesses need to collect information about their clients to be able to deliver services. That’s a fact. It just so happens that they have a new, quick and easy way to do it: the internet. Connecting your account through a secure digital channel simply makes more sense than filling paper forms with sensitive information or sending tax returns by email.

Being worthy of consumers’ trust is actually what makes us exist.

Respecting your privacy and handling your information with care is built into literally everything we do.

Even our coffee supplier was vetted.

“Well I don’t see my parents connecting their bank account any time soon.”

Consumers digitally sharing the information held by their bank to other financial providers of their choice is far from a marginal trend.

There’s a need for that. Financial providers need your information to verify who you are and understand your financial situation — always have, always will. But right now smart companies are making a better use of that information to create awesome features, lower their fees and provide a more personalized experience.

Flinks is enabling these changes by running a technology similar to what’s being used across North America by millions of consumers to connect with their favorite financial apps.

We believe you should be in control of your financial information. Flinks allows you to choose with whom you want to share it.

In fact, allowing consumers to share their financial information digitally is part of a movement happening everywhere in the world. It goes under the name of “open banking”, but it should really be called “consumer-directed finance”.

You might also like

How Fintechs Should Tackle Security: 5 Pillars of Our Security Strategy

When consumers’ data security is at stake, rigorous risk management is the name of the game — read on, this might help you build your own security strategy.